91752 Residential Real Estate Market Update (Jurupa Valley-Eastvale) – March 2024

The 91752-zip code, located in Riverside County, California, encompasses a small part of Eastvale (east of Hamner Avenue) and the western part of Jurupa Valley (Mira Loma area). The history of the ’52 zip code is closely tied to the development of these communities. Here’s a brief overview:

Throughout the 19th and early 20th centuries, the area was predominantly agricultural. It was known for its dairy farms and fields of crops, which benefited from the region’s fertile soil and favorable climate.

After World War II and into the 20th century, the region began to transform like many areas in Southern California. The growth of the Los Angeles metropolitan area, transportation improvements, and the increasing demand for suburban housing led to the development of residential communities, eventually becoming the cities of Eastvale and Jurupa Valley.

Today, the 91752-zip code is characterized by its suburban residential communities, commercial developments, and remaining agricultural areas. It reflects the more significant trends in Southern California’s Inland Empire – a shift from rural to suburban and urban landscapes.

The history of the 91752-zip code is a microcosm of the broader changes in Southern California – from indigenous lands to agricultural heartland to a thriving suburban area. It reflects the dynamic and ever-evolving nature of the region.

The following data is not intended to be a comparative market analysis for any one particular home but instead gives a general valuation for homes in each of the 12 specified areas and the entire residential areas located in the 91752-zip code.

For a detailed and personalized market analysis of your home, or if you have any questions, please get in touch with me.

Manny Barba,

Broker-Attorney-Realtor®

DRE #00879806

951-990-3998

mail@mbliverealty.com

MB Live Realty, Inc.

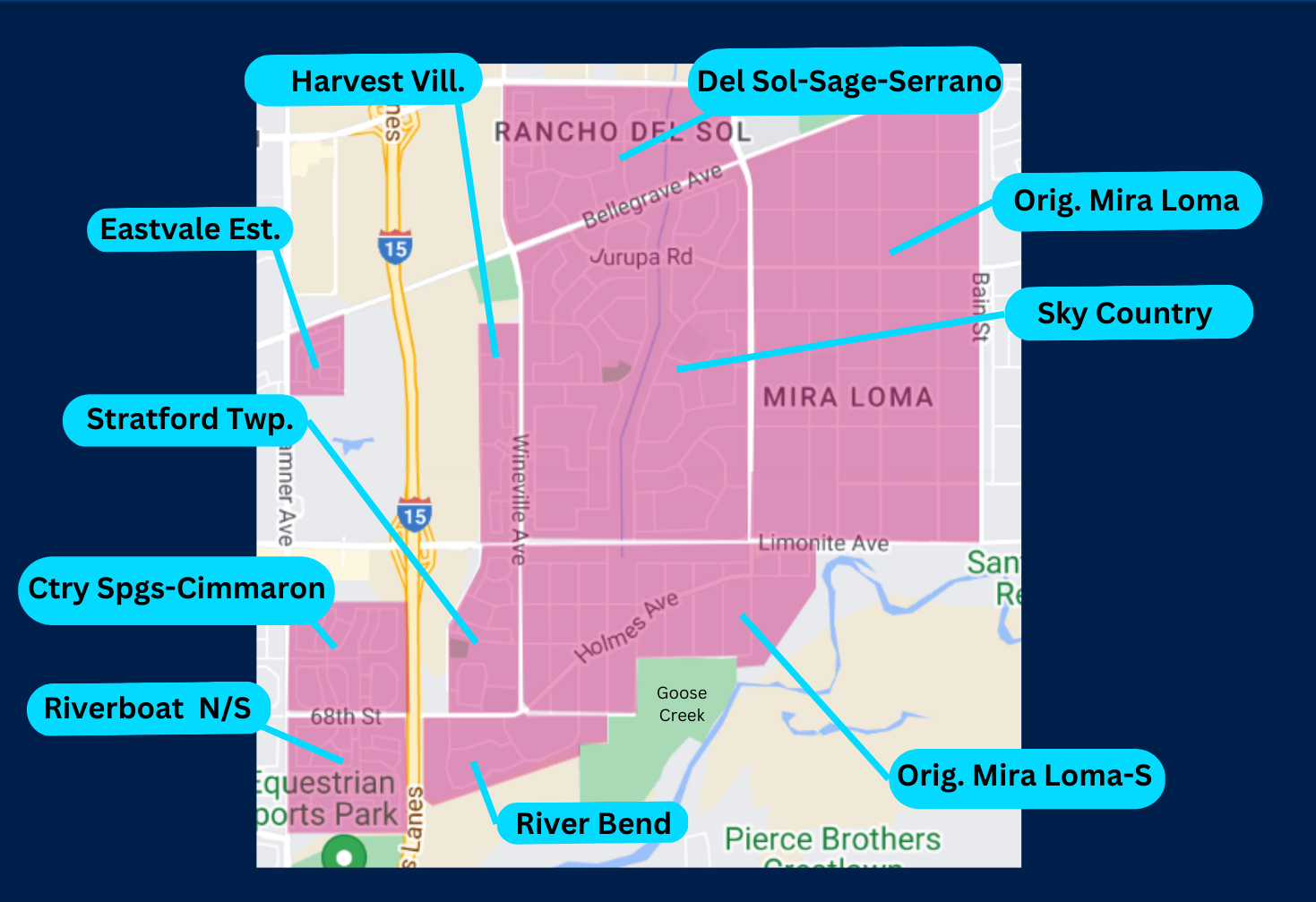

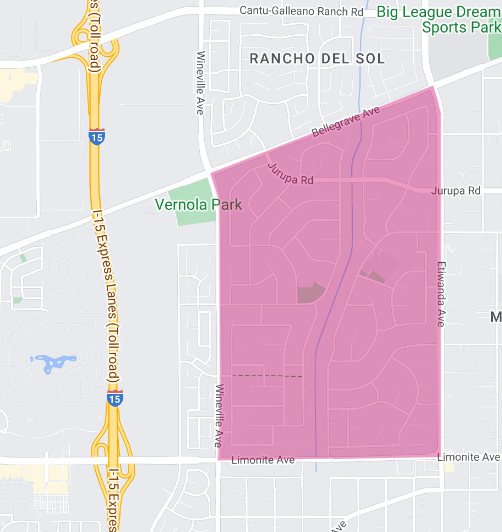

Area 1: Rancho Del Sol-Sage Pointe-Serrano Ranch area of homes,

(Western portion of Jurupa Valley 91752 )

As we close out March 2024, the Rancho Del Sol-Sage-Serrano Ranch residential area presents a nuanced real estate landscape, revealing trends that offer a mix of opportunities and challenges for buyers and sellers alike. This report aims to dissect the current market dynamics, shedding light on the shifting patterns and what they signify for those engaged in the local real estate market.

At the end of the month, the area had only 5 active listings, a 37.5% reduction from the previous year. This decline indicates a tightening market, where potential buyers may find fewer options available, potentially leading to increased competition for desirable homes.

In contrast, new listings saw a significant upswing, with 5 new properties entering the market, representing a substantial 150% increase from the previous year. This influx of new listings suggests that while the overall inventory remains lower than in the past, sellers are becoming more inclined to list their properties, providing prospective buyers a fresh batch of options.

The months’ supply of inventory stands at 2.2 months, reflecting a 24.1% decrease from last year. This decrease points towards a market moving faster than in the previous year, with properties being absorbed at a quicker pace, yet it still offers a relatively balanced dynamic between supply and demand.

Sales activity in the area has shown positive growth, with 2 closed sales occurring, a 60% increase from the previous year. This rise in sales activity, despite the lower inventory, underscores a sustained interest and demand within the Rancho Del Sol-Sage-Serrano Ranch area, indicating a healthy market pulse.

The average days on the market for properties sold has dramatically decreased to 28 days, down 49.1% from last year. This faster sales pace suggests that properties are moving more quickly through the market, likely due to strong buyer interest and the competitive nature of the available inventory.

Financially, the market dynamics are complex. The list-to-sold price percentage now stands at 100.5%, a 4.1% increase from the previous year. This indicates that, on average, homes are selling slightly above their asking price. This metric points to a competitive market environment where buyers are willing to pay premium prices for desirable homes.

However, the average sales price experienced a slight decline, settling at $878,500, which is a 3.2% decrease from the previous year. This reduction in average sales price might reflect a variance in the types of properties sold or perhaps a subtle shift in market conditions, suggesting that while demand remains strong, buyers may be more discerning in their purchasing decisions.

The average price per square foot saw a modest increase, rising to $287, a 2.5% change from last year. This increase in price per square foot, despite the drop in average sales price, could indicate a continued valuation of properties in the area, albeit with nuances in the size and type of properties being transacted.

In summary, the Rancho Del Sol-Sage-Serrano Ranch area’s real estate market is characterized by a reduction in active listings but a significant increase in new listings, suggesting a dynamic market with new opportunities for buyers. The increase in closed sales and a faster sales pace highlight strong demand, while the mixed financial indicators reflect a market in transition.

For buyers, the current environment offers new listings to consider, albeit in a competitive setting. Sellers, on the other hand, can benefit from a market where properties are selling relatively quickly, often at or above the asking price, although strategic pricing and understanding market dynamics remain crucial. Navigating this market effectively will require a keen understanding of these trends and an agile approach to real estate transactions.

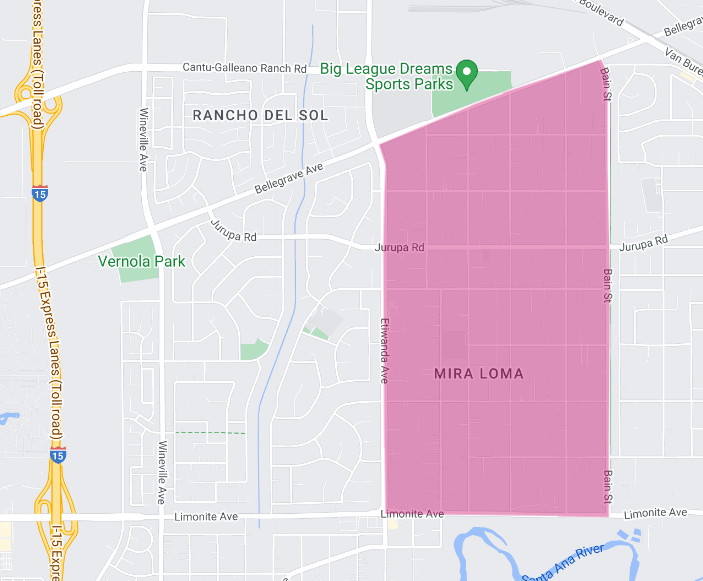

Area 2: Central Mira Loma (original)

(Western portion of Jurupa Valley 91752)

Ending March 2024, the original Mira Loma residential area has been unique, illustrating a market at a standstill in terms of new and active listings, yet showing significant changes in property values from the previous year. This report aims to dissect the current state of the market, offering insights into what these developments may mean for potential buyers and sellers in the area.

Remarkably, there were no active listings at the end of March 2024, marking a complete depletion of inventory from the previous year. This unprecedented situation of having zero new listings also indicates a halt in market activity, with no new properties being introduced for sale. The absence of any months’ supply of inventory data further emphasizes the complete lack of market movement in terms of listings.

Equally notable is the absence of closed sales during the month, a stark contrast to the previous year and an indicator of the standstill affecting the Original Mira Loma market. Without any transactions, there is no available data for average days on the market or list-to-sold price percentage, metrics that typically help gauge market health and buyer-seller dynamics.

Despite the lack of activity in listings and sales, the financial metrics reveal a different story. The average sales price in the area, calculated using a rolling 3-month average, stands at $830,000. This represents a substantial 34.3% increase from the previous year, indicating significant appreciation in property values despite the current market inactivity. This increase could reflect a range of factors, including previous demand trends, the intrinsic value of the area, and possibly limited supply over the past months.

Similarly, the average price per square foot has risen to $453, calculated using a rolling 3-month average, marking a 17.1% increase from last year. This growth further underscores the rising property values in Original Mira Loma, suggesting that while the market might be quiet in terms of sales and listings, the area remains highly valued and potentially lucrative for those who own property here.

In summary, the original Mira Loma residential real estate market presents a complex picture for March 2024. The complete absence of active and new listings, alongside a lack of closed sales, points to a unique period of inactivity. However, the significant appreciation in average sales prices and price per square foot reflects a strong undercurrent of value growth.

For homeowners in the original Mira Loma area, this might represent an opportune moment to assess the potential of their property investments. Potential buyers, on the other hand, will need to stay alert for any new listings, given the area’s demonstrated desirability and value appreciation. Moving forward, monitoring the market for signs of renewed activity will be crucial for all stakeholders.

Area 3: Sky Country,

(Western portion of Jurupa Valley 91752 )

As we conclude March 2024, the Sky Country residential area exhibits intriguing market dynamics, revealing both the opportunities and challenges facing buyers and sellers. This report aims to navigate through the current trends, providing a comprehensive overview of the real estate landscape in Sky Country.

The month ended with 2 active listings available, marking a 33.3% decrease from the same period last year. This reduction in active listings indicates a tighter market, potentially leading to increased competition among buyers for the limited inventory available. The scarcity of options could pressure buyers to make quicker decisions to secure properties in this sought-after area.

Interestingly, the number of new listings introduced to the market remained stable, with 2 properties coming up for sale, mirroring the activity from the previous year. This consistency in new listings suggests a steady interest among sellers to engage with the market, offering fresh opportunities for buyers despite the overall lower inventory levels.

The months’ supply of inventory has seen a slight decrease to 1.0 month, a 23.1% drop from the previous year, signaling a market that is moving quickly. Properties are being absorbed at a faster rate, indicating a seller’s market where demand outstrips supply, possibly leading to competitive bidding situations.

Sales activity remained consistent, with 3 closed sales reported, matching the volume from the previous year. This stability in sales volume, despite the lower inventory, underscores a sustained demand within the Sky Country area, reflecting the community’s enduring attractiveness.

However, the average days on the market for sold properties has seen a significant increase, jumping to 30 days, up 328.6% from the previous year. This substantial rise suggests that while demand remains strong, properties are taking longer to sell, potentially due to pricing strategies, buyer deliberation, or a mismatch in market expectations.

Financial metrics offer a mixed picture. The list-to-sold price percentage now stands at 103.3%, a 3.9% increase from the previous year, indicating that, on average, homes are selling for more than their asking price. This trend points to a competitive market where buyers are willing to pay premiums for desired properties.

The average sales price increased modestly to $753,333, a slight 1.1% rise from the previous year. This growth, while modest, indicates a steady appreciation in property values in Sky Country, suggesting that the area continues to be a valuable and desirable place to live.

Conversely, the average price per square foot experienced a decline, falling to $413, a 6.3% decrease from last year. This drop may reflect changes in the types of properties sold, varying buyer preferences, or other market conditions influencing the valuation of square footage.

In summary, the Sky Country residential real estate market presents a landscape characterized by decreased inventory but stable new listings, suggesting a dynamic environment with ongoing opportunities. The increase in average days on the market indicates a shift in sales dynamics, while the rise in the list-to-sold price percentage and a slight increase in average sales price reflect a competitive and valuable market.

The current conditions underscore the importance of decisiveness for buyers. Sellers can capitalize on the strong demand but may need to calibrate their expectations regarding the time to close a sale. As we move forward, understanding and navigating these market dynamics will be crucial for achieving success in the Sky Country area.

Area 4: Mira Loma – South (original)

(Western portion of Jurupa Valley 91752)

March 2024 marks a notable period for the original Mira Loma-South residential area, characterized by an unprecedented standstill in market activity, juxtaposed with shifts in property value metrics from the previous year. This report aims to provide an insightful overview of the current state of the real estate market in this unique community, highlighting the challenges and considerations for stakeholders.

The market has experienced a complete cessation of activity in terms of new and active listings, with both metrics falling to zero. This represents a 100% decrease in end-of-month active listings from the previous year and no change in new listings, indicating a stagnation in market dynamics. The absence of inventory contributes to a lack of market fluidity, leaving potential buyers without options in this area and sellers with no avenue to list their properties.

With no inventory available, the calculation of the months’ supply of inventory is not applicable, underscoring the unusual market conditions faced by the Original Mira Loma-South area. Similarly, the lack of closed sales, which decreased by 100% from the previous year, further emphasizes the complete halt in transactional activity. This absence of sales activity precludes the availability of data for average days on the market and the list to sold price percentage, critical indicators that typically offer insights into market health and buyer-seller negotiations.

Despite the standstill in listings and sales, financial metrics derived from a rolling 12-month average present a narrative of valuation changes. The average sales price in the Original Mira Loma-South area stands at $666,250, reflecting a 7.2% decrease from the previous year. This reduction in average sales price indicates a downward adjustment in property values, potentially influenced by broader market conditions or shifts in buyer preferences.

Furthermore, the average price per square foot has experienced a significant decline, dropping to $391. This 13.3% decrease from the previous year suggests a depreciation in the valuation of living space within the area, possibly resulting from evolving market dynamics or changes in the types of properties that were sold prior to the current inactivity.

In summary, the Original Mira Loma-South residential real estate market presents a scenario of total inactivity, with no listings or sales occurring in March 2024. Despite this stagnation, the observed decreases in average sales price and price per square foot highlight underlying shifts in property value.

For current homeowners, this situation warrants close monitoring of market trends for future opportunities to sell or leverage their property investments. Potential buyers, meanwhile, will need to wait for new listings to emerge or consider exploring adjacent areas for available properties.

As the market navigates through this period of inactivity, understanding the implications of these valuation changes will be crucial for all stakeholders looking to engage with the Original Mira Loma-South real estate landscape in the future.

Area 5: River Bend Homes

(Western Edge of Jurupa Valley 91752)

March 2024 in the River Bend residential area has unveiled a market characterized by significant shifts in inventory levels, sales dynamics, and property values, painting a complex picture for those navigating the real estate landscape. This report aims to dissect these trends, offering clarity and insight into the current state of the market.

At the end of the month, the area witnessed a decrease in active listings, with just 2 properties available. This represents a 33.3% decline from the previous year, signaling a tighter market with fewer homes available. This reduction in active listings indicates a potential increase in competition among buyers for the available properties.

Similarly, new listings saw a parallel reduction, dropping by 33.3% from the previous year, with 2 new properties being introduced to the market. This decrease in new listings further emphasizes the constrained supply of homes, which could lead to heightened demand for those that do become available.

The months’ supply of inventory has narrowed to 1.0 months, marking a significant 41.2% decrease from last year. This reduction highlights a market moving at an accelerated pace, with homes being absorbed quickly as they enter the market. The limited inventory suggests a competitive environment, favoring sellers in transaction negotiations.

Sales activity remained steady, with 1 closed sale reported, mirroring the activity from the previous year. The consistency in closed sales, despite the reduced inventory, indicates a sustained interest and demand within the River Bend area.

The average days on market for properties sold saw a drastic reduction to just 4 days, down 98.4% from the previous year. This dramatic decrease in the time it takes to sell a property suggests a highly competitive market, with homes selling almost immediately after listing. This fast-paced sales environment underscores the urgency among buyers to secure properties in this sought-after area.

Financial metrics reveal a mixed landscape. The list-to-sold price percentage now stands at 102.3%, a 3.0% increase from last year. This indicates that, on average, homes are selling for slightly above their asking price. This metric points to a competitive bidding environment, where buyers are willing to pay premiums to secure their desired homes.

The average sales price in the River Bend area has risen to $940,000, reflecting a substantial 16.0% increase from the previous year, based on a rolling 3-month average. This increase highlights significant appreciation in property values, benefiting homeowners and attracting potential investors.

Conversely, the average price per square foot experienced a decrease, falling to $297, a 13.4% drop from last year. This decline may reflect changes in the types of properties sold or a shift in buyer preferences, but it contrasts with the overall increase in average sales prices.

In summary, the River Bend residential real estate market is experiencing a phase of tightened inventory and rapid sales, with properties moving quickly and often selling for above asking price. The significant appreciation in average sales price, coupled with a reduction in the average price per square foot, presents a nuanced view of the market.

For buyers, the current conditions necessitate quick action and flexibility, while sellers are positioned advantageously in a market that favors their interests. Understanding these dynamics will be crucial for effectively navigating the River Bend real estate market in the coming months.

Area 6: Riverboat Dr. Area Homes

(Western Edge of 91752 ZIP Code, Eastvale, CA)

March 2024 has brought forward a set of intriguing dynamics to the residential area adjacent to Riverboat Drive, both to the north and south, underlining a market that is rapidly evolving, yet remains robust in its fundamentals. This report is crafted to navigate through these changes, offering a comprehensive analysis to understand the current real estate landscape in this coveted area.

The market witnessed a reduction in the number of active listings at the end of March, with just one property available. This represents a 50% decrease from the previous year, signaling a significantly tighter market. Such a reduction in active listings typically indicates a scarcity of available properties, potentially leading to increased competition among buyers.

Despite the sharp decrease in active listings, new listings remained constant with one new property entering the market, matching the activity level from the previous year. This stability in new listings, amidst an overall decrease in active inventory, suggests a cautious but continuous interest among sellers in capitalizing on the current market conditions.

The months’ supply of inventory has seen a notable reduction to 0.8 months, marking a 38.5% decrease from last year. This accelerated depletion of inventory signifies a market moving at a brisk pace, with available properties being absorbed quickly upon listing. Such conditions often lead to a seller’s market, where demand outweighs supply, potentially driving up property values.

Sales activity declined, with two closed sales, a 33.3% decrease from the previous year. This drop in sales volume, despite a decrease in inventory, might reflect various factors, including buyer selectiveness or external market influences impacting transaction completion.

The average days on the market for sold properties dramatically decreased to just 2 days, an 88.2% reduction from the previous year. This significant acceleration in sales pace underscores the high demand and competitiveness of the market, with properties selling almost immediately after listing. Such rapid transactions highlight the urgency among buyers to secure properties in this desirable location.

Financially, the market demonstrates robust growth. The list-to-sold price percentage has increased to 102.3%, a 1.9% rise from the previous year. This indicates that homes are selling for slightly above their asking price on average. This trend points to a competitive bidding environment, where buyers are willing to pay premiums for desirable properties.

The average sales price saw a substantial increase, reaching $960,000, reflecting an 18.5% appreciation from the previous year. This significant rise in property values benefits homeowners and attracts potential buyers, showcasing the area’s continued desirability and the strength of the real estate market.

Conversely, the average price per square foot experienced a decrease, falling to $268, a 10.1% drop from last year. This reduction may reflect a variety of factors, including changes in the types of properties sold or a shift in market preferences, but it contrasts with the overall increase in average sales prices.

In summary, the residential area adjacent to Riverboat Drive is experiencing a market characterized by decreased inventory and an extremely rapid pace of sales, with properties often selling above the asking price. The significant increase in average sales prices and a reduction in the average price per square foot presents a nuanced picture.

The current market conditions necessitate swift action and flexibility for buyers, whereas sellers are advantageously positioned in a competitive market environment. Understanding and navigating these dynamics will be crucial for stakeholders looking to engage with this vibrant real estate market.

Area 7: Country Springs/ Cimmaron Ranch

(Western Edge of 91752 ZIP Code, Eastvale, CA)

March 2024 in the Country Springs-Cimmaron Ranch residential area presents a distinct set of market dynamics, reflecting a significant transition in property availability and sales activity compared to the previous year. This report delves into these trends, offering insights into this community’s evolving real estate landscape.

Remarkably, the area experienced a total depletion of active listings by the end of March, marking a 100% decrease from the year prior. This complete absence of available inventory signifies a unique market scenario, pausing the inflow of new buying opportunities and signaling a highly constrained environment for potential buyers.

Despite the stark drop in active listings, the market did see the introduction of 1 new listing during the month. However, without comparative data from the previous year for new listings, it’s challenging to gauge the trend in seller behavior or market fluidity based on this singular entry.

The lack of active listings also renders the calculation of months’ supply of inventory inapplicable, leaving a gap in understanding the balance between supply and demand based on traditional metrics. This situation underscores the current scarcity of homes in the area, which could have various implications on market dynamics and pricing.

Sales activity has halved, with only 1 closed sale reported, a 50% decrease from the previous year. This reduction in sales volume and the absence of active listings highlight a significant slowdown in market transactions, potentially indicating a cautious or wait-and-see approach among buyers and sellers.

The average days on the market for properties sold decreased significantly to just 8 days, down 55.6% from last year. Despite the reduced volume, this rapid pace of sales suggests that demand for homes in the Country Springs-Cimmaron Ranch area remains strong, with properties that do enter the market moving quickly to closing.

Financial metrics provide a mixed perspective. The list-to-sold price percentage slightly decreased to 98.9%, a marginal 0.1% drop from the previous year, indicating that homes are selling very close to their asking prices. This slight adjustment suggests a slight shift towards buyers in negotiation dynamics, though sellers are still achieving near-full asking prices.

The average sales price saw a modest increase, rising to $892,500, based on a rolling 3-month average. This 3.9% appreciation from the previous year reflects a stable growth in property values within the area, indicating a continued desirability and investment potential in the Country Springs-Cimmaron Ranch community.

Conversely, the average price per square foot decreased, falling to $272, a 4.9% drop from the previous year. This decline may suggest changes in the types or sizes of properties being sold or indicate a shift in market valuations, contrasting with the overall increase in average sales prices.

In summary, the Country Springs-Cimmaron Ranch residential area is experiencing significant market constraints, marked by a complete lack of active listings and a reduction in closed sales. Despite these challenges, the rapid pace of sales for properties that do come to market and the modest increase in average sales prices underscore a persistent demand.

The current market conditions for potential buyers necessitate swift action upon the arrival of new listings. Though facing a unique market scenario, sellers can find solace in stable property values and the potential for quick sales at competitive prices. As we move forward, the evolution of this market will require close monitoring to adapt to its dynamic nature.

Area 8: Stratford Township Homes

(Western Edge of Jurupa Valley 91752)

March 2024 has unfolded with a distinct set of developments within the Stratford Township residential area, reflecting a market that is both evolving and facing challenges in terms of listings and sales dynamics. This report aims to dissect these trends, offering a nuanced overview of the state of real estate in this sought-after community.

The area witnessed a decrease in the number of active listings at the end of March, with only one property available. This marks a 50% reduction from the previous year, indicating a significantly tighter market. Such a decrease in active listings suggests a scarcity of available homes, which could potentially increase competition among buyers for the limited options available.

Notably, there were no new listings introduced to the market this month, representing a 100% drop from last year. This absence of new listings further exacerbates the already constrained inventory, potentially leading to heightened demand for any properties that do become available in the future.

The months’ supply of inventory has been reduced to 0.7 months, a 46.2% decrease from the previous year. This significant reduction in inventory levels underscores a market moving at a brisk pace, with available properties being absorbed quickly upon listing. The low inventory level suggests a competitive environment, likely favoring sellers in transaction negotiations.

Sales activity remained steady, with one closed sale reported, mirroring the activity from the previous year. The consistency in closed sales, despite the reduced inventory, indicates a sustained interest and demand within the Stratford Township area, reflecting the enduring attractiveness of the community.

However, the average days on the market for properties sold saw a significant increase to 36 days, up 100% from the previous year. This increase suggests that, while demand remains strong, properties are taking longer to sell, potentially due to pricing strategies, buyer deliberation, or a mismatch in market expectations.

Financially, the market demonstrates a positive trajectory. The list-to-sold price percentage slightly decreased to 97.6%, a 1.8% drop from the previous year. This indicates that homes are selling close to their asking price, albeit with a slight adjustment toward buyer negotiation advantage.

The average sales price saw a modest increase, reaching $826,600, based on a rolling 6-month average. This 5.1% appreciation from the previous year underscores the area’s desirability and the overall strength of the real estate market, benefiting homeowners and attracting potential buyers.

Similarly, the average price per square foot experienced a notable increase, rising to $291, a 13.2% rise from the previous year. This increase further demonstrates the robust market performance and significant appreciation in property values, highlighting the attractiveness of the Stratford Township area as a place to live and invest.

In summary, the Stratford Township residential area is navigating a period marked by decreased inventory and a lack of new listings while maintaining a healthy sales pace and appreciating property values. The increase in average days on the market indicates a shift in sales dynamics, while the growth in average sales price and price per square foot reflects a competitive and valuable market.

For buyers, the current market conditions necessitate quick action and flexibility, whereas sellers are advantageously positioned in a market that remains strong despite inventory challenges. Understanding and navigating these market dynamics will be crucial for stakeholders looking to engage effectively with the Stratford Township real estate market.

AREA 9: Eastvale Estates (Bellegrave Ave./Hamner Ave/)

(Western Edge of 91752 ZIP Code, Eastvale, CA)

March 2024 in the Eastvale Estates residential area presents a stable yet intriguing snapshot of the real estate market, characterized by steady listing activity but a notable absence of closed sales during the period. This report aims to provide a comprehensive analysis of the current market conditions, offering insights and guidance for those looking to engage with the Eastvale Estates real estate landscape.

The market has maintained a consistent level of activity in terms of listings, with 2 active listings available at the end of the month. This stability in inventory suggests a balanced inflow and outflow of properties within the market, providing potential buyers with a steady stream of options. Similarly, new listings for the month also stood at 2, indicating a regular pace of homeowners deciding to sell their properties, contributing to the dynamic market environment.

The months’ supply of inventory remained stable at 2 months, reflecting a market that has neither tightened nor loosened compared to the previous year. This equilibrium suggests a balanced market, where supply and demand are relatively in sync, potentially offering neither party a distinct advantage in negotiations.

Notably, there were no closed sales recorded during the month, marking a period of inactivity in terms of transactions. This absence of sales could be attributed to various factors, including possible mismatches between buyer expectations and available properties or broader economic conditions influencing buyer readiness.

Due to the lack of closed sales, there is no available data for average days on market or the list to sold price percentage. These metrics, which typically offer insights into the pace of the market and negotiation dynamics, cannot be evaluated for this period, leaving a gap in understanding the current transaction trends in Eastvale Estates.

Financially, the market demonstrates a significant valuation with an average sales price of $800,000, calculated using a rolling 6-month average. This valuation underscores the area’s desirability and the premium nature of properties within Eastvale Estates, reflecting a strong investment potential for homeowners and buyers alike.

The average price per square foot stands at $342, also calculated on a rolling 6-month average. This metric further illustrates the market’s robustness, indicating the value buyers place on living space within this sought-after community.

In summary, the Eastvale Estates residential area exhibits a market characterized by stable listing activity but a pause in sales transactions during March 2024. The maintained inventory levels and consistent new listings indicate ongoing seller engagement, yet the absence of closed sales highlights a period of buyer hesitation or potential market recalibration. The stable average sales price per square foot reflects a strong market foundation, suggesting continued interest and value in the Eastvale Estates area.

The current conditions may offer potential buyers opportunities to find desirable properties, while sellers should be prepared for possible fluctuations in buyer activity. Navigating this market will require close attention to emerging trends and strategic decision-making to capitalize on the opportunities within Eastvale Estates.

Area 10: Harvest Villages at Vernola Ranch

(Western Edge of Jurupa Valley 91752)

March 2024 in the Harvest Villages residential area presents a market experiencing shifts in listing activity and sales dynamics, reflecting both the challenges and opportunities within the current real estate landscape. This report provides a detailed analysis of these trends, offering valuable insights to buyers, sellers, and market watchers alike.

The area saw a decrease in the number of end-of-month active listings, with only 2 properties available, representing a 33.3% reduction from the previous year. This decline in active listings indicates a tighter market with fewer options for potential buyers, potentially leading to increased competition for available homes.

The trend of decreasing availability is further evidenced by the number of new listings, which halved to just 1 new property entering the market, a 50% drop from last year. This reduction in new listings contributes to the constrained supply, possibly affecting buyer choice and delaying purchase decisions for those seeking specific property types or features.

The months’ supply of inventory has decreased to 1.5 months, a 25% reduction from the previous year. This tighter supply underscores a market moving at a faster pace than before, with properties being absorbed more quickly. However, this trend towards a seller’s market is contrasted by the lack of closed sales during the month, which fell by 100% from the previous year, indicating a standstill in transaction activity.

Due to the absence of closed sales, there is no available data for average days on the market or the list to-sold price percentage. These metrics typically help gauge the speed of sales and negotiation dynamics but remain unreported due to the current inactivity in completed transactions.

Financially, the market shows signs of continued strength and desirability. The average sales price in Harvest Villages has seen a modest increase, reaching $845,000, based on a rolling 6-month average. This 1.1% appreciation from the previous year reflects a stable market valuation, suggesting that properties in the area maintain their appeal and investment potential despite the current sales slump.

Furthermore, the average price per square foot experienced a significant rise, reaching $293, an 11.8% increase from last year. This notable increase highlights the area’s continued attractiveness and the premium placed on living space within this community, possibly driven by buyer preferences for quality and location.

In summary, the Harvest Villages residential area navigates a period of reduced listing activity coupled with a temporary pause in sales transactions. The decrease in active and new listings points to a market with limited supply, while the lack of closed sales signals a temporary mismatch between buyer and seller expectations or broader market hesitations. Despite these challenges, the average sales price and price per square foot appreciation indicate a resilient market foundation.

Buyers may find opportunities in the limited inventory available, whereas sellers must carefully consider timing and pricing strategies in a shifting market landscape. As we move forward, adapting to these dynamics will be key for successful real estate endeavors in Harvest Villages.

Area 11: Mira Loma Village,

(North-Western portion of Jurupa Valley 91752)

March 2024 in the Mira Loma Village residential area is characterized by a unique scenario where market activity in new and active listings and closed sales has come to a standstill. Despite this pause in transactional activity, significant information can be gleaned from the valuation trends over the past year. This report seeks to navigate these dynamics, providing insights into the implications for stakeholders within this community.

The area has not experienced any change in the number of end-of-month active listings from the previous year, with the count remaining at zero. Similarly, no new listings were introduced to the market this month, mirroring the status from last year. The absence of active and new listings indicates a market with no immediate opportunities for potential buyers to enter or for sellers to list new properties.

Given the lack of active and new listings, the concept of months’ supply of inventory is not applicable, as there is effectively no inventory available in the market. This situation is highly unusual and suggests a market experiencing a significant pause in both supply and demand.

Sales activity has also remained static, with no closed sales occurring this month, consistent with the previous year’s activity—or lack thereof. The absence of closed sales means there are no available data for average days on the market or the list-to-sold price percentage, which typically offers insights into market velocity and negotiation dynamics.

Despite this pause in market transactions, financial metrics over a rolling 12-month average provide a stark contrast, showcasing substantial appreciation in property values within the area. The average sales price has witnessed an exceptional increase, reaching $597,500, representing an 81.1% surge from the previous year. This dramatic rise in average sales price underscores the significant appreciation in property values, reflecting a strong underlying demand for homes in Mira Loma Village and the community’s attractiveness as a desirable place to live.

Similarly, the average price per square foot has seen a notable increase, rising to $453, up 41.6% from last year. This increase further emphasizes the premium placed on property within the area, indicating robust valuation trends despite the current standstill in market activity.

Historical sales data since January 1, 2023, provide additional context. Two homes sold over the past year—one in February 2023 for $615,000, slightly above its list price of $610,000, and another in August 2023 for $580,000, significantly above its list price of $525,000. These transactions highlight the market’s competitive nature when properties are available, with buyers willing to pay premiums for desired homes.

In summary, the Mira Loma Village residential area presents a market paradox: there is no current transactional activity yet significant appreciation in property values over the past year. The substantial increases in the average sales price and price per square foot reflect a latent demand and the community’s inherent value.

For potential buyers, the current pause suggests the importance of readiness for when new listings eventually enter the market. For homeowners, the appreciation trends highlight the potential value of their properties should they choose to sell. Navigating this unique market landscape will require patience and strategic planning, with a close watch on emerging opportunities in the future.

Area 12: Homestead,

(North-Western portion of Jurupa Valley 91752)

As we conclude March 2024, the Homestead residential area presents a nuanced picture of its real estate market, characterized by a mix of stability in listings and significant changes in sales activity and property values. This report aims to provide an insightful overview of these dynamics, offering valuable guidance for stakeholders interested in this community.

The number of active listings at the end of March remained stable with 1 property available, mirroring the situation from the previous year. This consistency in active listings suggests a steady state in terms of available inventory for potential buyers, although the singular listing indicates a tightly constrained market with limited options.

New listings declined, with only 1 new property entering the market, marking a 50% decrease from the previous year. This reduction in new listings contributes to the already limited inventory, potentially increasing competition for any properties that do become available.

The months’ supply of inventory decreased slightly to 0.5 months, down 16.7% from a year ago. This metric underscores an accelerated market, with inventory levels suggesting a highly competitive environment likely favoring sellers. However, the absence of closed sales during the month, a significant departure from the previous year, highlights a pause in transactional activity, possibly due to mismatches between buyer expectations and available properties or broader market conditions.

Due to the lack of closed sales, there is no available data for average days on market or the list to sold price percentage. These metrics, which typically offer insights into the pace of the market and negotiation dynamics, cannot be evaluated for this period, leaving a gap in understanding the current transaction trends in Homestead.

Despite the pause in sales activity, financial metrics over a rolling 3-month average reveal noteworthy trends. The average sales price has increased, reaching $586,667, representing a 4.0% appreciation from the previous year. This rise in average sales price reflects stable growth in property values, indicating the area’s desirability and the overall strength of the real estate market in Homestead.

Similarly, the average price per square foot experienced a significant rise, reaching $494, up 10.3% from last year. This increase further highlights the robust market performance and appreciation in property values, showcasing the premium placed on living space within the Homestead area.

In summary, the Homestead residential area is navigating through a period marked by a stable number of listings but a noticeable pause in sales transactions. The maintenance of inventory levels and the absence of closed sales point to a unique market scenario. Despite these challenges, the average sales price and price per square foot appreciation underscore a strong market foundation, suggesting continued interest and value in Homestead properties.

For potential buyers, the current market conditions necessitate swift action upon the emergence of new listings, whereas sellers might find the appreciation trends promising should market activity resume. Navigating this market effectively will require a keen understanding of these dynamics and a strategic approach to real estate transactions in the Homestead area.

******

As a real estate broker, understanding the above-nuanced market shifts is key to providing informed advice and strategy to sellers throughout the 91752 zip code area.

Contact me to understand how the above trends can impact your real estate decisions. I provide expert guidance and strategic insights and can guide you through these interesting times in real estate.

Manny Barba

Broker-Attorney-Realtor®

951-990-3998

MB Live Realty, Inc.

Note: All data in this report is from California Regional Multiple Listing Service (CRMLS) All information should be independently reviewed and verified for accuracy. This report is for informational purposes only and not intended as financial or investment advice.

![]()

{kind=link}

{kind=link}

{kind=link}

No Comments